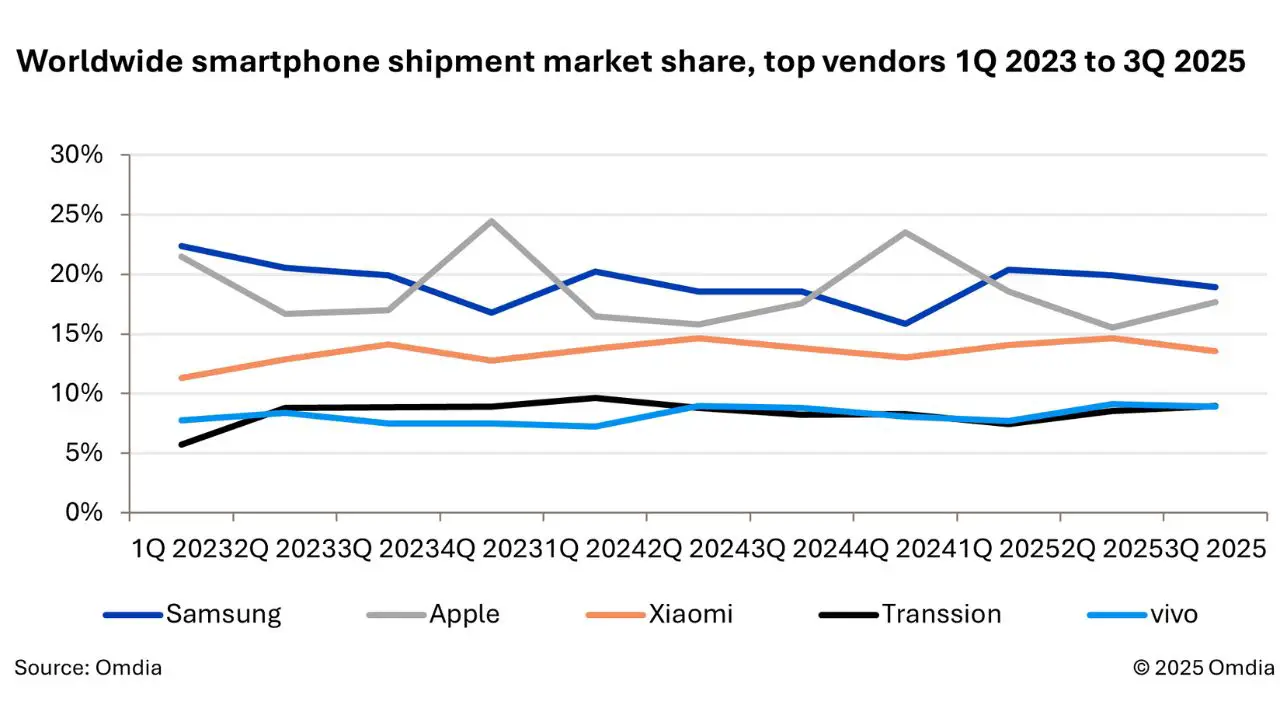

- Global smartphone sales Q3 2025 climbed to 320.1 million units, marking a steady 3% year-on-year recovery after a sluggish start to the year.

- Samsung retained its lead with 60.6 million shipments and a 19% share, while Apple and Xiaomi followed closely amid rising competition.

- Emerging markets like Africa and Asia-Pacific fueled most of the global growth, even as mid-range smartphone sales continued to decline.

The latest report from Omdia says the global smartphone market finally started to bounce back in the third quarter of 2025. Between July and September, around 320.1 million smartphones were shipped across the world, which is a 3% increase compared to last year. It’s not a huge jump, but it shows that things are moving in the right direction after a weak start earlier this year.

What’s interesting is that the growth is not equal across all price segments. The market is kind of split into two ends. The cheapest phones, usually under 100 dollars, and the most expensive ones, over 700 dollars, are doing really well. The mid-range phones are struggling a bit, and that’s been the case for a while now.

Global smartphone sales Q3 2025 show signs of recovery

Samsung keeps the top spot

Samsung still holds the crown as the top smartphone maker globally. It shipped 60.6 million devices in Q3 2025 and managed to grab a 19% market share, growing 6% compared to the same period last year.

Samsung’s strategy of focusing on both high-end foldables like the Galaxy Z Fold7 and Flip7, and on budget-friendly models such as the Galaxy A07 and A17, seems to be working perfectly. The company’s performance in regions like the Middle East and Asia-Pacific played a huge role in this success.

Apple and Xiaomi follow closely

Right behind Samsung, Apple secured second place with 56.5 million shipments, which gave it an 18% share of the market. The interesting part is that the base iPhone 17 performed much better than many expected. It’s one of the reasons why Apple saw a 4% yearly growth in Q3 2025.

Xiaomi came third with 43.4 million units shipped, holding 14% market share. Its growth was smaller, around 1% year-on-year, but still a positive sign. Xiaomi did face lower sales in China after the end of government subsidy programs, but it managed to recover with solid numbers in the Asia-Pacific region.

Transsion and Vivo push forward

The biggest surprise this quarter came from Transsion Holdings, the company behind Infinix, Tecno, and Itel. It saw a huge 12% year-on-year growth, shipping 28.6 million units. Transsion’s major win came from Africa, where smartphone shipments jumped by 25% compared to last year. This rise helped Transsion move up to fourth place globally.

Vivo was right behind, also shipping around 28.5 million units, with a 9% market share. Vivo did especially well in India and Southeast Asia, where its budget models are quite popular.

Emerging markets take the lead

When you look at the overall picture, it’s clear that emerging markets are doing the heavy lifting for the global smartphone industry right now. Africa saw the strongest growth, followed by the Asia-Pacific region, which grew about 5% year-on-year. On the other hand, North America and China didn’t perform as well, with shipments slightly declining.

This shift shows how more developing countries are becoming the new hotspots for smartphone growth. Brands like Transsion and Vivo are smartly focusing on these markets, offering affordable devices with decent features that attract millions of first-time smartphone users.

Top 5 global smartphone vendors in Q3 2025

| Rank | Vendor | Shipments (Millions) | Market Share | YoY Growth | Main Growth Driver |

|---|---|---|---|---|---|

| 1 | Samsung | 60.6 | 19% | 6% | Foldables (Z series) & A series |

| 2 | Apple | 56.5 | 18% | 4% | Strong base iPhone 17 demand |

| 3 | Xiaomi | 43.4 | 14% | 1% | Asia-Pacific recovery |

| 4 | Transsion | 28.6 | 9% | 12% | Africa market growth |

| 5 | Vivo | 28.5 | 9% | 5% | Strong performance in India & Asia-Pacific |

The mid-range struggle continues

Looking ahead, the mid-range segment still faces challenges. There are rising component costs and supply issues, and companies might have to pass those costs to buyers. That could mean higher prices in the coming months.

Analysts believe that this trend will keep the market divided into two clear parts. On one side, budget phones that people buy for value and basic use. On the other side, premium flagships that attract users looking for high-end specs and design. The middle ground just doesn’t seem to fit as much anymore.

Overall, the smartphone sales Q3 2025 results show that the market is recovering, but in a very uneven way. Budget and premium phones are driving most of the sales, while the mid-range category continues to lose steam. As we move into the next quarter, it will be interesting to see if manufacturers find a way to bring balance back or if this “all or nothing” trend continues.